How are you using predictive models to assess the mortality impact of underwriting without fluids?

Since mortality is a lagging indicator and is often not credible, due to the large number of deaths required, we often need to use mortality proxies to supplement actual measured mortality. Predictive models tend to be far superior to any other methodology to connect inputs available at time of underwriting with outcomes (deaths).

Having said that, there are many different types of predictive models and the most suitable approach depends on the circumstances. We have a team of highly qualified statisticians who work with underwriters and actuaries to determine the best approach.

There is a false presumption that today’s underwriting approach appropriately classifies all risks.

How close are we to getting to preferred risk pricing using an accelerated underwriting approach?

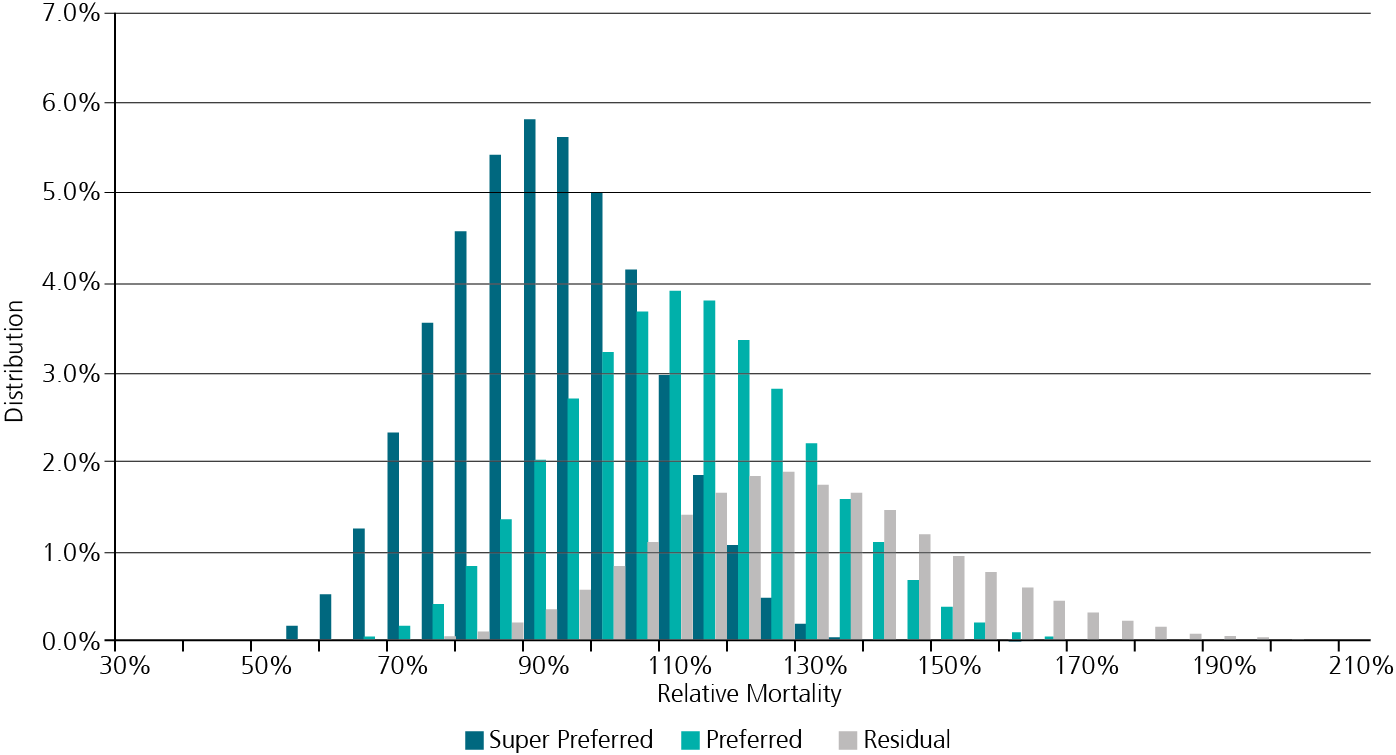

We are already there – it is entirely possible to define preferred and super preferred risk classes using new sources, such as credit based mortality risk scores. The issue the market still has to overcome is that the risks traditionally assigned to preferred classes by biometric centric selection approaches will be different risks than those identified by other methods. Innovative carriers will come to accept non-traditional underwriting practices and new products are sure to follow.

Why is it important to start the accelerated underwriting development process with a clear understanding of business objectives?

While the seeming similarity of selection approaches for many US companies makes it tempting to think that all are mostly the same, the reality is that different markets, differences in distribution, product and specific underwriting selection make every scenario different from the next. One size approach certainly does not fit all, so defining the most important business objectives is key. Accelerated underwriting is simply one additional way to accomplish some of these objectives.

What new data sources are too good to be true – or still a long way away?

Due to the non-structured format and lack of standardization among vendors, EHR (Electronic Health Records) may still be years away from being consumed by an automated engine. Although a PDF version of an applicant’s medical record may currently be available through EHR vendors, it does not help with ‘speed to issue’.

The holy grail of complete automation, including attending physician statements via electronic health records, is still out of practical reach.